Breaking News! Cedars-Sinai Joins Blue Shield PPO Network—March 2015

In-Demand Hospital finally becomes accessible to many residents who live on Los Angeles’ West side.

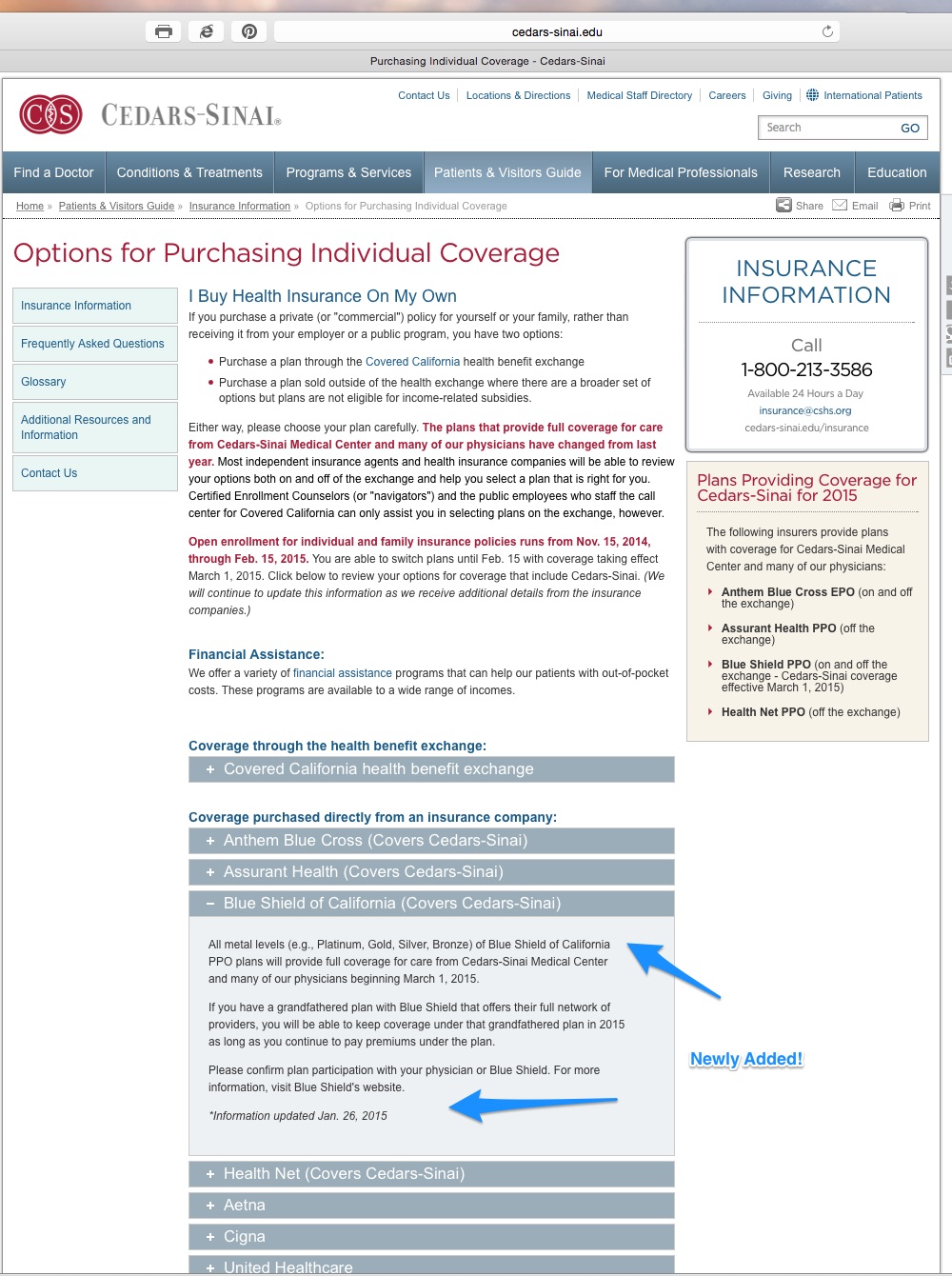

On January 26, Cedars’ website was updated to show Blue Shield’s Individual and Family Plan (IFP) PPO options as “in-network”.

Screenshot of Cedars’ Insurance Page taken on 1/29/15.

These plans are available both “on-exchange” (through a Covered California Certified Agent) and “off-exchange” (directly through a Blue Shield agent). There is no difference between “on” and “off” exchange plans; simply a different method of submitting an application for coverage. (Purchasing an on-exchange plan is the only method to apply for a tax credit/subsidy, however).

Blue Shield’s plans have been the lowest-cost PPO plans available in LA County for the last two years, but the lack of access to Cedars-Sinai was previously a disadvantage that was a deal breaker to many people who live nearby in West Hollywood, Beverly Hills, and Los Angeles, or who value the hospital’s excellent reputation.

Now, many people may consider switching plans to take advantage of the premium savings. However, the opportunity to change plans (or enroll in a new plan) closes with the end of Open Enrollment on February 15, 2015.

Blue Shield also offers excellent Dental and Vision Insurance options, but only when enrolling “Off-exchange”. (Covered California has plans to offer Dental options, but the rollout has been delayed.

If you would like to explore your options with Blue Shield (or any other insurance company) call me at 626-676-3466 and I’ll be happy to provide advice and assistance.

Or, click THIS LINK or the photos below to explore your options online.