Could Consumers Actually Benefit from the Silver Surcharge?

Silver 70 plans through Covered California are being surcharged.

How to avoid the surcharge.

There are several methods.

First, do you even need to avoid it? Covered California plans that are being substantially subsidized with an Advance Premium Tax Credit (APTC) don’t need to avoid the surcharge. If fact, these people could actually benefit from the surcharge.

The reason is due to the complicated formula for calculating the tax credit, which sets the Silver plans as the basis. By surcharging just the Silver plans, everyone who qualifies for a tax credit (based on income) will receive a larger, more generous tax credit (APTC).

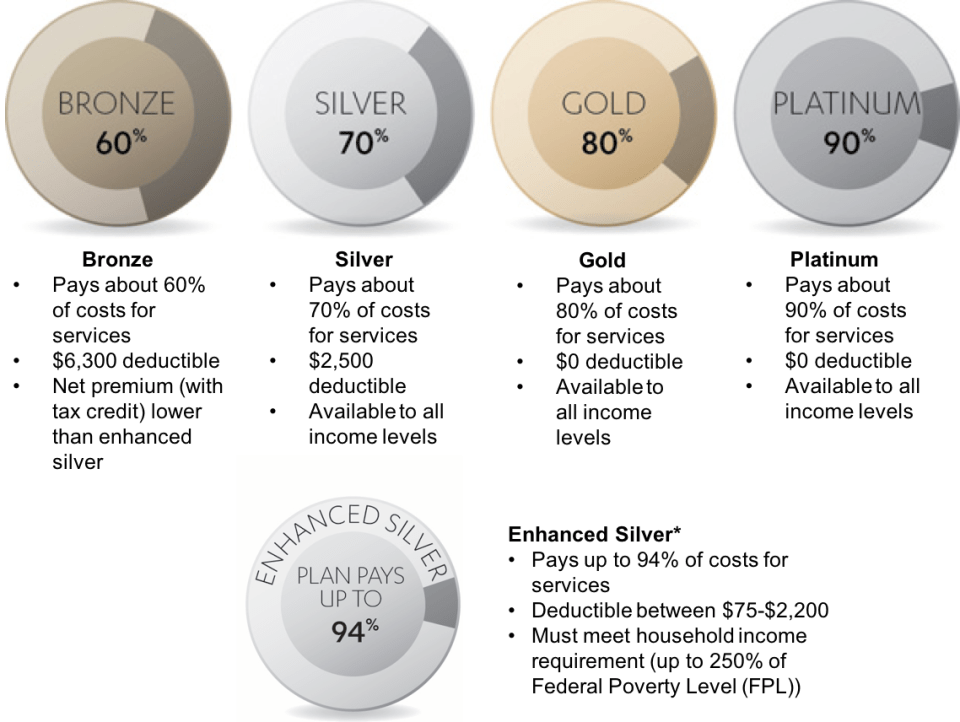

The tax credit (APTC) can be applied to Bronze, Gold, and Platinum plans, as well as Silver plans.

Bronze, Gold, and Platinum plans are not being surcharged. Just the Silver plans that were purchased through Covered California are being surcharged.

Therefore, some people who have incomes low enough to qualify for a substantial tax credit (APTC), but high enough to be ineligible for the Silver 94 or the Silver 87, will find the Gold, Bronze, and Platinum plans to be a relatively better deal as a result of the more generous ax credit (APTC).

But, do you have enough coverage?

Be careful about purchasing less or more coverage than you actually need merely for the purpose of avoiding the surcharge.

The Bronze plans are much less coverage. Be careful about the Bronze plans! The Bronze plans have a very high deductible, and you could wind up with lots of medical bills that you didn’t anticipate. In general, the Bronze plans are for risk-tolerant, healthy folks who don’t actually plan to fill prescription drugs, have labs, x-rays, MRIs, surgeries, etc and won’t be pregnant, and they have cash reserves of several thousand dollars to pay for unexpected medical bills that arise.

The Gold and Platinum plans have more coverage than Silver 70 and Silver 73 plans.

Thinking about your coverage needs:

How have you used your healthcare in the past year? Did you find that you were paying more out-of-pocket than you expected when you visited the doctors, had lab tests, bought pills, or had surgery? In 2018, do you expect any surgical procedures, hospital visits, or illness?

Email or call me at (626) 765-4495 we can discuss which plan is right for you.

What needs to be done now?

Call me at (626) 765-4495 to review your renewal options.

If you need to apply for new coverage altogether, or switch from an On-Exchange Covered California plan (the “Marketplace”), November 1st is the start of Open Enrollment, that’s when we’ll be able to submit new applications that take effect starting January 2018.

If you need assistance, please plan to call me in November to enroll in a new plan.

Rates and Doctor Networks are changing. Give me a call for assistance! As a Covered California Certified Insurance Agent (CIA), I can help you:

- Renew or Change your plan.

- Make sure you’re getting the best value.

- Help you qualify for the correct Tax Credit / Subsidy. (And avoid mistakes that might haunt you at tax time!).

- Know which plans have your doctors & hospitals “in-network,” and which plans do not.

- Figure out billing issues and answer other questions.

- Provide an alternative to waiting on hold with Customer Service hotlines.

- Troubleshoot.

No Cost to You – No Extra Fees.

CALL:

626-765-4495

626-765-4495

Some California consumers received

Some California consumers received